Filed pursuant to Rule 424(b)(3)

Registration No. 333-230669

PROSPECTUS/OFFER TO EXCHANGE

CONCRETE PUMPING HOLDINGS, INC.

Offer to Exchange Warrants to Acquire Shares of Common Stock

of

Concrete Pumping Holdings, Inc.

for

Shares of Common Stock of Concrete Pumping Holdings, Inc.

and

Consent Solicitation

THE OFFER PERIOD (AS DEFINED BELOW) AND WITHDRAWAL RIGHTS WILL EXPIRE AT 11:59 P.M., EASTERN DAYLIGHT TIME, ON APRIL 26, 2019, OR SUCH LATER TIME AND DATE TO WHICH WE MAY EXTEND.

Terms of the Offer and Consent Solicitation

Until the Expiration Date (as defined below), we are offering to the holders of our warrants (the “warrants”) to purchase shares of common stock, par value $0.0001 per share (“common stock”), of Concrete Pumping Holdings, Inc. (the “Company”, “we”, “us” and “our”) the opportunity to receive 0.2105 shares of common stock in exchange for each outstanding public warrant tendered and 0.1538 shares of common stock in exchange for each outstanding private placement warrant tendered pursuant to the offer (the “Offer”). The Offer is being made to:

|

● |

All holders of our publicly traded warrants (the “public warrants”) to purchase shares of our common stock, which were originally issued as warrants to purchase shares of common stock of Industrea Acquisition Corp. (“Industrea”) in connection with Industrea’s initial public offering on August 1, 2017 (the “Industrea IPO”) and automatically became exercisable for shares of our common stock on December 6, 2018 in connection with the consummation of the Business Combination (as defined herein), each of which are exercisable for one share of our common stock for a purchase price of $11.50 per share in accordance with its terms. |

|

● |

All holders of certain of our warrants to purchase common stock (the “private placement warrants” and together with the public warrants, the “warrants”) that were issued in a private placement concurrently with the Industrea IPO, which entitle such warrant holders to purchase one share of our common stock for a purchase price of $11.50 per share in accordance with its terms. |

Our common stock is listed on The Nasdaq Capital Market (“Nasdaq”) under the symbol “BBCP,” and our public warrants are quoted on the OTC Pink marketplace maintained by OTC Market Groups, Inc. under the symbol “BBCPW.” The warrants are governed by the warrant agreement, dated as of July 26, 2017, by and between the Company and Continental Stock Transfer & Trust Company (the “Warrant Agreement”). As of April 1, 2019, 23,000,000 public warrants and 11,100,000 private placement warrants were outstanding. Pursuant to the Offer, we are offering up to an aggregate of 4,841,500 shares of our common stock in exchange for the public warrants, or 0.2105 shares for every public warrant, and 1,707,180 shares of common stock in exchange for the private placement warrants, or 0.1538 shares for every private placement warrant. CFLL Sponsor Holdings LLC, an affiliate of Argand Partners, LP, holds 97.5% of our outstanding private placement warrants and has committed to tender such warrants pursuant to the Offer. See the section of this Prospectus/Offer to Exchange entitled “The Offer and Consent Solicitation—Transactions and Agreements Concerning Our Securities—Tender and Support Agreement.”.

No fractional shares of common stock will be issued pursuant to the Offer. In lieu of issuing fractional shares, any holder of warrants who would otherwise have been entitled to receive fractional shares pursuant to the Offer will, after aggregating all such fractional shares of such holder, be paid in cash (without interest) in an amount equal to such fractional part of a share multiplied by the last sale price of our common stock on Nasdaq on the last trading day of the Offer Period (as defined below). Our obligation to complete the Offer is not conditioned on the receipt of a minimum number of tendered warrants.

Concurrently with the Offer, we are also soliciting consents (the “Consent Solicitation”) from holders of the public warrants to amend the Warrant Agreement (the “Warrant Amendment”), which governs all of the warrants, to permit the Company to require that each warrant that is outstanding upon the closing of the Offer be converted into 0.1895 shares of common stock, which is a ratio 10% less than the exchange ratio applicable to the public warrants in the Offer. Pursuant to the terms of the Warrant Agreement, the consent of holders of at least 65% of the outstanding public warrants is required to approve the Warrant Amendment. Therefore, one of the conditions to the adoption of the Warrant Amendment is the receipt of the consent of holders of at least 65% of the outstanding public warrants. You may not consent to the Warrant Amendment without tendering your public warrants in the Offer and you may not tender your public warrants without consenting to the Warrant Amendment. The consent to the Warrant Amendment is a part of the letter of transmittal and consent relating to the public warrants, and therefore by tendering your public warrants for exchange you will be delivering to us your consent. You may revoke your consent at any time prior to the Expiration Date (as defined below) by withdrawing the public warrants you have tendered in the Offer.

The Offer and Consent Solicitation is made solely upon the terms and conditions in this Prospectus/Offer to Exchange and in the related letter of transmittal and consent (as it may be supplemented and amended from time to time, the “Letter of Transmittal and Consent”). The Offer and Consent Solicitation will be open until 11:59 p.m., Eastern Daylight Time, on April 26, 2019 or such later time and date to which we may extend (the period during which the Offer and Consent Solicitation is open, giving effect to any withdrawal or extension, is referred to as the “Offer Period,” and the date and time at which the Offer Period ends is referred to as the “Expiration Date”). The Offer and Consent Solicitation is not made to those holders who reside in states or other jurisdictions where an offer, solicitation or sale would be unlawful.

We may withdraw the Offer and Consent Solicitation only if the conditions to the Offer and Consent Solicitation are not satisfied or waived prior to the Expiration Date. Promptly upon any such withdrawal, we will return the tendered warrants to the holders (and the consent to the Warrant Amendment will be revoked).

You may tender some or all of your warrants into the Offer. If you elect to tender warrants in response to the Offer and Consent Solicitation, please follow the instructions in this Prospectus/Offer to Exchange and the related documents, including the Letter of Transmittal and Consent. If you tender warrants, you may withdraw your tendered warrants at any time before the Expiration Date and retain them on their current terms or amended terms if the Warrant Amendment is approved, by following the instructions in this Prospectus/Offer to Exchange. In addition, tendered warrants that are not accepted by us for exchange by April 26, 2019 may thereafter be withdrawn by you until such time as the warrants are accepted by us for exchange. If you withdraw the tender of your public warrants, your consent to the Warrant Amendment will be withdrawn as a result.

Warrants not exchanged for shares of our common stock pursuant to the Offer will remain outstanding subject to their current terms or amended terms if the Warrant Amendment is approved. We reserve the right to redeem any of the warrants, as applicable, pursuant to their current terms at any time, including prior to the completion of the Offer and Consent Solicitation, and if the Warrant Amendment is approved, we intend to require the conversion of all outstanding warrants to shares of common stock as provided in the Warrant Amendment.

The Offer and Consent Solicitation is conditioned upon the effectiveness of a registration statement on Form S-4 that we filed with the U.S. Securities and Exchange Commission (the “SEC”) regarding the shares of common stock issuable upon exchange of the warrants pursuant to the Offer. This Prospectus/Offer to Exchange forms a part of the registration statement.

Our board of directors has approved the Offer and Consent Solicitation. However, neither we nor any of our management, our board of directors, or the information agent, the exchange agent or the dealer manager for the Offer and Consent Solicitation is making any recommendation as to whether holders of warrants should tender warrants for exchange in the Offer and consent to the Warrant Amendment in the Consent Solicitation. Each holder of a warrant must make its own decision as to whether to exchange some or all of its warrants and consent to the Warrant Amendment.

All questions concerning the terms of the Offer and Consent Solicitation should be directed to the dealer manager:

UBS SECURITIES LLC

1285 Avenue of the Americas

New York, New York 10019

Attention: Equity Capital Markets

(212) 713-2626

All questions concerning exchange procedures and requests for additional copies of this Prospectus/Offer to Exchange, the Letter of Transmittal and Consent or the Notice of Guaranteed Delivery should be directed to the information agent:

Morrow Sodali LLC

470 West Avenue

Stamford, Connecticut 06902

Individuals, please call toll-free: (800) 662-5200

Banks and brokerage firms, please call: (203) 658-9400

Email: BBCP.info@morrowsodali.com

We will amend our offering materials, including this Prospectus/Offer to Exchange, to the extent required by applicable securities laws to disclose any material changes to information previously published, sent or given to warrant holders.

The securities offered by this Prospectus/Offer to Exchange involve risks. Before participating in the Offer and consenting to the Warrant Amendment, you are urged to read carefully the section entitled “Risk Factors” included on page 17 in this Prospectus/Offer to Exchange.

Neither the SEC nor any state securities commission or any other regulatory body has approved or disapproved of these securities or determined if this Prospectus/Offer to Exchange is truthful or complete. Any representation to the contrary is a criminal offense.

Through the Offer, we are soliciting your consent to the Warrant Amendment. By tendering your warrants, you will be delivering your consent to the proposed Warrant Amendment, which consent will be effective upon our acceptance of the warrants for exchange.

The dealer manager for the Offer and Consent Solicitation is:

UBS Investment Bank

This Prospectus/Offer to Exchange is dated April 19, 2019

TABLE OF CONTENTS

|

1 |

|

|

2 |

|

|

3 |

|

|

6 |

|

|

13 |

|

|

16 |

|

|

17 |

|

|

37 |

|

|

57 |

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF THE COMPANY |

70 |

|

99 |

|

|

UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

100 |

|

112 |

|

|

119 |

|

|

126 |

|

|

135 |

|

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

139 |

|

141 |

|

|

141 |

|

|

141 |

|

|

F-1 |

ABOUT THIS PROSPECTUS/OFFER TO EXCHANGE

This Prospectus/Offer to Exchange is a part of the registration statement that we filed on Form S-4 with the U.S. Securities and Exchange Commission. You should read this Prospectus/Offer to Exchange, including the detailed information regarding the Company, common stock and warrants, and the financial statements and the notes that are included in this Prospectus/Offer to Exchange and any applicable prospectus supplement.

You should rely only on the information contained in this Prospectus/Offer to Exchange and in any accompanying prospectus supplement. We have not authorized anyone to provide you with information different from that contained in this Prospectus/Offer to Exchange. If anyone makes any recommendation or representation to you, or gives you any information, you must not rely upon that recommendation, representation or information as having been authorized by us. We and the dealer manager take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. You should not assume that the information in this Prospectus/Offer to Exchange or any prospectus supplement is accurate as of any date other than the date on the front of those documents. You should not consider this Prospectus/Offer to Exchange to be an offer or solicitation relating to the securities in any jurisdiction in which such an offer or solicitation relating to the securities is not authorized. Furthermore, you should not consider this Prospectus/Offer to Exchange to be an offer or solicitation relating to the securities if the person making the offer or solicitation is not qualified to do so, or if it is unlawful for you to receive such an offer or solicitation.

Unless the context requires otherwise, in this Prospectus/Offer to Exchange, we use the terms “the Company,” “CPH,” “our company,” “we,” “us,” “our,” and similar references to refer to Concrete Pumping Holdings, Inc. and its subsidiaries.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Prospectus/Offer to Exchange contains forward-looking statements. These forward-looking statements relate to expectations for future financial performance, business strategies or expectations for our business. Specifically, forward-looking statements may include statements relating to:

|

● |

the consummation of the Capital Acquisition and the benefits of the Business Combination and the Capital Acquisition; |

|

● |

our future financial performance following the Business Combination and the Capital Acquisition; |

|

● |

the Equity Offering and the planned debt financing in connection with the Capital Acquisition; |

|

● |

our business strategy; |

|

● |

changes in the market for our products; |

|

● |

expansion plans and opportunities; and |

|

● |

other statements preceded by, followed by or that include the words “may,” “can,” “should,” “will,” “estimate,” “plan,” “project,” “forecast,” “intend,” “expect,” “anticipate,” “believe,” “seek,” “target” or similar expressions. |

You should not place undue reliance on these forward-looking statements in deciding whether to invest in our securities. As a result of a number of known and unknown risks and uncertainties, our actual results or performance may be materially different from those expressed or implied by these forward-looking statements. Some factors that could cause actual results to differ include:

|

● |

the risk that the Capital Acquisition disrupts current plans and operations; |

|

● |

the ability to recognize the anticipated benefits and synergies of the Business Combination and the Capital Acquisition, which may be affected by, among other things, competition and the ability of the combined business to grow and manage growth profitably; |

|

● |

costs related to the Business Combination and the Capital Acquisition and the subsequent integration of Capital; |

|

● |

our ability to finance the Capital Acquisition as planned, including our ability to consummate the debt financing and Equity Offering as contemplated; |

|

● |

changes in applicable laws or regulations; |

|

● |

fluctuations in the U.S. and/or global stock markets; |

|

● |

the possibility that we may be adversely affected by other economic, business, and/or competitive factors; and |

|

● |

other risks and uncertainties described in this Prospectus/Offer to Exchange under “Risk Factors.” |

Such risks and uncertainties also include those set forth under “Risk Factors” herein. Our forward-looking statements speak only as of the time that they are made and do not necessarily reflect our outlook at any other point in time, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing our views as of any subsequent date. We do not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

“A. Crawford” means A. Keith Crawford.

“Argand” means Argand Partners, LP.

“Argand Investor” means Argand Partners Fund, LP.

“ASC” means ASC Equipment, LP, a Texas limited partnership.

“Business Combination” means the transactions contemplated by the Merger Agreement consummated on December 6, 2018, which included the CPH Merger and the Industrea Merger.

“Board” means the board of directors of the Company.

“Brundage-Bone” means Brundage-Bone Concrete Pumping Holdings, Inc., a Colorado corporation

“Buyers” means CPHA LLC and Brundage-Bone.

“Bylaws” means our second amended and restated bylaws as currently in effect.

“Camfaud” means Camfaud Group Limited, the name under which the Company operates in the United Kingdom (“U.K.”).

“Capital Acquisition” means the transactions contemplated by the Interest Purchase Agreement.

“Capital Companies” means MCS, ASC and CP.

“CFLL Sponsor” or the "Sponsor" means CFLL Sponsor Holdings, LLC (formerly known as Industrea Alexandria LLC), a Delaware limited liability company.

“Charter” means our amended and restated certificate of incorporation as currently in effect.

“Closing” means the closing of the Business Combination.

“Closing Date” means December 6, 2018, the closing date of the Business Combination.

“Code” means the Internal Revenue Code of 1986, as amended.

“common stock” means the common stock, par value $0.0001 per share, of the Company.

“Company” means Concrete Pumping Holdings, Inc., a Delaware corporation (formerly known as Concrete Pumping Holdings Acquisition Corp.) and the successor entity to Industrea.

“CP” means Capital Pumping, LP, a Texas limited partnership.

“CPH” means Brundage-Bone Concrete Pumping Holdings, Inc. (formerly known as Concrete Pumping Holdings, Inc.), a Delaware corporation, which merged with and into a wholly owned subsidiary of the Company at the Closing and survived the merger as a wholly owned indirect subsidiary of the Company.

“CPHA LLC” means CPH Acquisition, LLC, a Delaware limited liability company and wholly owned subsidiary of Brundage-Bone.

“CPH Merger” means the merger of a wholly owned indirect subsidiary of the Company with and into CPH, with CPH surviving the merger as a wholly owned indirect subsidiary of the Company at the Closing.

“CPH stockholders” means certain holders of CPH’s capital stock prior to the Business Combination.

“Consent Solicitation” means the solicitation of consent from the holders of the public warrants to approve the Warrant Amendment.

“CR LLC” means Capital Rentals, LLC, a Texas limited liability company.

“CTCS” means Central Texas Concrete Services, LLC, a Texas limited liability company.

“DGCL” means the Delaware General Corporation Law.

“Eco-Pan” means the Company’s brand of concrete waste management services provider.

“Equity Offering” means the Company’s proposed offering of equity securities to fund the Capital Acquisition.

“ERISA” means the Employment Retirement Income Security Act of 1974.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“Expiration Date” means 11:59 p.m., Eastern Daylight Time on April 26, 2019.

“Industrea” means Industrea Acquisition Corp., a Delaware corporation and the predecessor entity to the Company.

“Industrea Merger” means the merger of a wholly owned indirect subsidiary of the Company with and into Industrea, with Industrea surviving the merger as a wholly owned indirect subsidiary of the Company at the Closing.

“Initial Stockholders” means the CFLL Sponsor and Industrea’s independent directors collectively

“Interest Purchase Agreement” means that certain Interest Purchase Agreement, dated as of March 18, 2019, by and among the Company, the Buyers, the Capital Companies and the Sellers, pursuant to which, subject to the satisfaction or waiver of certain conditions set forth therein, (i) Brundage-Bone will purchase all of the outstanding (x) limited partnership interests in CP and ASC from A. Crawford and (y) limited liability company interests in MCS from M. Crawford, and (ii) CPHA LLC will purchase all of the general partnership interests in CP and ASC from CR LLC and CTCS, respectively.

“Industrea IPO” means Industrea’s initial public offering of units, which closed on August 1, 2017.

“Letter of Transmittal and Consent” means the letter of transmittal and consent (as it may be supplemented and amended from time to time) related to the Offer and Consent Solicitation.

“M. Crawford” means Melinda Crawford.

“Merger Agreement” means that certain Agreement and Plan of Merger, dated as of September 7, 2018, by and among the Company, Industrea, CPH, certain subsidiaries of the Company, and PGP Investors, LLC, solely in its capacity as the initial Holder Representative, as amended on each of October 30, 2018 and November 16, 2018.

“MCS” means MC Services, LLC, a Texas limited liability company.

“Nasdaq” means The Nasdaq Capital Market.

“Offer” means the opportunity to receive (i) 0.2105 shares of common stock in exchange for each of our outstanding public warrants and (ii) 0.1538 shares of common stock for each of our outstanding private placement warrants.

“Offer Period” means the period during which the Offer and Consent Solicitation is open, giving effect to any extension.

“OTC Pink” means the OTC Pink marketplace maintained by OTC Market Groups, Inc.

“proxy statement/prospectus” means the proxy statement/prospectus included in the Company’s registration statement on Form S-4 (File No. 333-227259), as amended and supplemented, originally filed with the SEC on September 10, 2018.

“private placement warrants” means the 11,100,000 warrants issued to CFLL Sponsor in a private placement simultaneously with the closing of the Industrea IPO.

“public warrants” means the 23,000,000 redeemable warrants included in the units issued in the Industrea IPO, each of which is exercisable for one share of common stock at an exercise price of $11.50 per share, in accordance with its terms.

“SEC” means the U.S. Securities and Exchange Commission.

“Section 203” means Section 203 of the DGCL.

“Securities Act” means the Securities Act of 1933, as amended.

“Sellers” means the Capital Companies, CR LLC, CTCS, A. Crawford and M. Crawford.

“Series A preferred stock” means the Company’s Series A Zero-Dividend Convertible Perpetual Preferred Stock.

“Stockholders Agreement” means the Stockholders Agreement, dated December 6, 2018, by and among the Company and the Investors party thereto.

“Tender and Support Agreement” means the Tender and Support Agreement, dated April 1, 2019, between the Company and CFLL Sponsor, pursuant to which CFLL Sponsor has agreed to tender its private placement warrants pursuant to the Offer and consent to the Warrant Amendment pursuant to the Consent Solicitation.

“warrants” means the public warrants and the private placement warrants.

“Warrant Agreement” means that Warrant Agreement, dated as of July 26, 2017, by and between Industrea and Continental Stock Transfer & Trust Company.

“Warrant Amendment” means the amendment to the Warrant Agreement permitting the Company to require that each outstanding warrant be converted into 0.1895 shares of common stock, which is a ratio 10% less than the exchange ratio applicable to the Offer.

In this Prospectus/Offer to Exchange, unless otherwise stated, the terms “the Company,” “we,” “us” or “our” refer to Concrete Pumping Holdings, Inc. and its subsidiaries.

The Offer and Consent Solicitation

This summary provides a brief overview of the key aspects of the Offer and Consent Solicitation. Because it is only a summary, it does not contain all of the detailed information contained elsewhere in this Prospectus/Offer to Exchange or in the documents included as exhibits to the registration statement that contains this Prospectus/Offer to Exchange. Accordingly, you are urged to carefully review this Prospectus/Offer to Exchange in its entirety (including all documents filed as exhibits to the registration statement that contains this Prospectus/Offer to Exchange, which exhibits may be obtained by following the procedures set forth herein in the section entitled “Where You Can Find Additional Information”).

Summary of The Offer and Consent Solicitation

|

The Company |

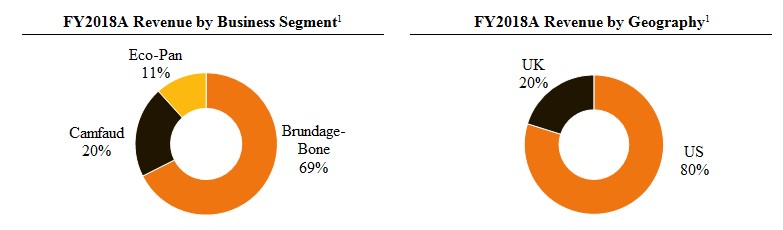

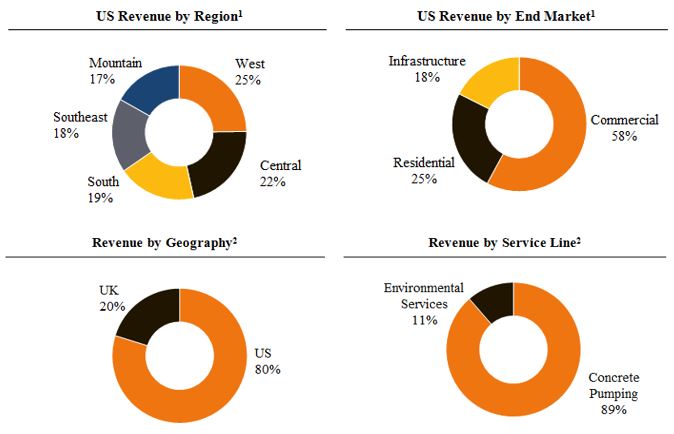

We are a leading provider of concrete pumping services and concrete waste management services in the U.S. and U.K. based on fleet size, operating under what we believe are the only established national brands in both geographies – Brundage-Bone Concrete Pumping, Inc. (“Brundage-Bone”) for concrete pumping and Eco-Pan, Inc. (“Eco-Pan”) for waste management services in the U.S. and Camfaud Group Limited (“Camfaud”) in the U.K. Concrete pumping is a highly specialized method of concrete placement that requires skilled operators to position a truck-mounted, fully-articulating boom for precise delivery of ready-mix concrete from mixer trucks to placing crews on a construction job site. In addition, proper concrete washout handling has become an increasing area of focus, with rising awareness of environmental factors. Our large fleet of specialized pumping equipment, washout pans and trucks, and highly-trained operators enable us to be the trusted provider of concrete placement and waste management solutions to our customers. We deliver and facilitate substantial labor cost savings, shortened concrete placement times, enhanced worksite safety, and efficient concrete washout containment, and thereby help improve the overall quality of construction projects. As of January 31, 2019, we operated a fleet of 951 units of equipment, with 673 experienced employees and 121 locations globally.

Industrea was incorporated in Delaware on April 7, 2017 as a blank check company formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses. The Company was incorporated on August 29, 2018 as a Delaware corporation solely for the purpose of effectuating the Business Combination, which was consummated on December 6, 2018. Upon the Closing, all outstanding shares of Industrea’s Class A common stock were exchanged on a one-for-one basis for shares of our common stock, and Industrea’s outstanding warrants were assumed by us and became exercisable for shares of our common stock on the same terms as were contained in such warrants prior to the Business Combination. By operation of Rule 12g-3(a) under the Exchange Act, the Company is the successor issuer to Industrea and has succeeded to the attributes of Industrea as the registrant, including Industrea’s SEC file number (001-38166) and CIK Code (0001703956). In connection with the Closing, we changed our name from “Concrete Pumping Holdings Acquisition Corp.” to “Concrete Pumping Holdings, Inc.” |

|

Recent Developments |

On March 18, 2019, we entered into the Interest Purchase Agreement with the Capital Companies, the Buyers and the Sellers, pursuant to which, subject to the satisfaction or waiver of certain conditions set forth therein, (i) Brundage-Bone will purchase all of the outstanding (x) limited partnership interests in CP and ASC from A. Crawford and (y) limited liability company interests in MCS from M. Crawford, and (ii) CPHA LLC will purchase all of the general partnership interests in CP and ASC from CR LLC and CTCS, respectively (the transactions contemplated by the Interest Purchase Agreement, the “Capital Acquisition”). As a result of the Capital Acquisition, each of the Capital Companies will become our wholly-owned indirect subsidiaries. The consideration for the Capital Acquisition will consist of an aggregate of $129.2 million payable in cash, subject to adjustments as described in the Interest Purchase Agreement. The Capital Acquisition is expected to close in the third quarter of fiscal year 2019, subject to regulatory approvals and other customary closing conditions. On March 26, 2019, the Federal Trade Commission granted early termination of the waiting period under the Hart-Scott-Rodino Act (the “HSR Act”) with respect to the Capital Acquisition. The Company expects to finance the acquisition through the Equity Offering and additional $40 million of borrowings under its Term Loan Agreement. This Offer is not contingent upon the closing of the Capital Acquisition.

On March 26, 2019, the Company and certain of its affiliates entered into an Amendment No. 1 to Term Loan Agreement, with Stifel Bank & Trust (“Stifel”) and Credit Suisse AG, Cayman Islands Branch (the “Administrative Agent”), pursuant to which Stifel and certain other lenders agreed to provide, subject to satisfaction of customary closing conditions, including the closing of the Capital Acquisition, incremental term loans in an aggregate amount up to $40 million (the “Amendment No. 1 Term Loans”), which shall be borrowed under, and have substantially the same terms as the term loans previously borrowed under the Term Loan Agreement, dated as of December 6, 2018, by and among the Company, certain of its affiliates, the Administrative Agent and each lender party thereto from time to time, for the purpose of financing a portion of the consideration payable in connection with the Capital Acquisition and the fees and expenses in connection therewith and in connection with the Amendment No. 1 Term Loans.

On April 15, 2019, the Company acquired Atlas Concrete Pumping Inc. (“Atlas”), a provider of concrete pumping services in Idaho, for a purchase price of approximately $3.8 million, payable in cash and common stock. |

|

Corporate Contact Information |

Our principal executive offices are located at 6461 Downing Street, Denver, Colorado 80229. Our telephone number is (303) 289-7497. Our website is located at www.concretepumpingholdings.com. The information contained on, or that may be accessed through, our website is not part of, and is not incorporated into, this Prospectus/Offer to Exchange or the registration statement of which it forms a part. |

|

Warrants that qualify for the Offer |

As of April 1, 2019, we had outstanding 34,100,000 warrants, consisting of 23,000,000 public warrants and 11,100,000 private placement warrants, each exercisable for one share of our common stock at a price of $11.50 per share, subject to adjustments pursuant to the Warrant Agreement. The public warrants were originally issued in connection with the Industrea IPO and the private placement warrants were originally issued in a private placement that closed concurrently with the Industrea IPO. Each of the public warrants and private placement warrants converted into warrants to purchase shares of our common stock on the same terms in connection with the Business Combination. Pursuant to the Offer, we are offering 0.2105 shares of our common stock in exchange for each outstanding public warrant, or 4,841,500 shares of common stock in the aggregate, and 0.1538 shares of our common stock in exchange for each outstanding private placement warrant, or 1,707,180 shares in the aggregate. Pursuant to the Tender and Support Agreement, CFLL Sponsor, which holds 97.5% of our outstanding private placement warrants, has agreed to tender such warrants pursuant to the Offer. |

|

Under the Warrant Agreement, we may call the public warrants for redemption at our option:

● in whole and not in part;

● at a price of $0.01 per warrant;

● upon not less than 30 days’ prior written notice of redemption (the “30-day redemption period”) to each warrantholder; and

● if, and only if, the reported last sale price of our common stock equals or exceeds $18.00 per share (as adjusted for stock splits, stock dividends, reorganizations, recapitalizations and the like) for any 20 trading days within a 30-trading day period ending three business days before we send the notice of redemption to the warrantholders.

The public warrants expire on December 6, 2023. |

|||

|

Market Price of Our Common Stock |

Our common stock is listed on Nasdaq under the symbol “BBCP,” and the public warrants are quoted on OTC Pink under the symbol “BBCPW.” See “The Offer and Consent Solicitation — Market Price, Dividends and Related Shareholder Matters.” |

|

The Offer |

Each public warrant holder who tenders public warrants for exchange pursuant to the Offer will receive 0.2105 shares of our common stock for each public warrant so exchanged and each holder of private placement warrants who tenders private placement warrants for exchange will receive 0.1538 shares of common stock for each private placement warrants so exchanged. No fractional shares of common stock will be issued pursuant to the Offer. In lieu of issuing fractional shares, any holder of warrants who would otherwise have been entitled to receive fractional shares pursuant to the Offer will, after aggregating all such fractional shares of such holder, be paid cash (without interest) in an amount equal to such fractional part of a share multiplied by the last sale price of our common stock on Nasdaq on the last trading day of the Offer Period. Our obligation to complete the Offer is not conditioned on the receipt of a minimum number of tendered warrants or the consummation of the Capital Acquisition.

Holders of the warrants tendered for exchange will not have to pay any of the exercise price for the tendered warrants in order to receive shares of common stock in the exchange. |

|

The shares of common stock issued in exchange for the tendered warrants will be unrestricted and freely transferable, as long as the holder is not an affiliate of ours and was not an affiliate of ours within the three months prior to the proposed transfer of such shares. |

|

The Offer is being made to all warrant holders except those holders who reside in states or other jurisdictions where an offer, solicitation or sale would be unlawful (or would require further action in order to comply with applicable securities laws). |

||

|

The Consent Solicitation |

In order to tender public warrants in the Offer and Consent Solicitation, holders are required to consent (by executing the Letters of Transmittal and Consent or requesting that their broker or nominee consent on their behalf) to an amendment to the Warrant Agreement governing the public warrants as set forth in the Warrant Amendment attached as Annex A. If approved, the Warrant Amendment would permit the Company to require that all warrants that are outstanding upon the closing of the Offer be converted into shares of common stock at a ratio of 0.1895 shares of common stock per public warrant (a ratio which is 10% less than the exchange ratio applicable to the Offer). Upon such conversion, no warrants will remain outstanding. |

|

|

Purpose of the Offer and Consent Solicitation |

The purpose of the Offer and Consent Solicitation is to attempt to simplify our capital structure and reduce the potential dilutive impact of the warrants, thereby providing us with more flexibility for financing our operations in the future. See “The Offer and Consent Solicitation — Background and Purpose of the Offer and Consent Solicitation.” |

|

|

Offer Period |

The Offer and Consent Solicitation will expire on the Expiration Date, which is 11:59 p.m., Eastern Daylight Time, on April 26, 2019, or such later time and date to which we may extend. All warrants tendered for exchange pursuant to the Offer and Consent Solicitation, and all required related paperwork, must be received by the exchange agent by the Expiration Date, as described in this Prospectus/Offer to Exchange. |

|

|

If the Offer Period is extended, we will make a public announcement of such extension by no later than 9:00 a.m., Eastern Daylight Time, on the next business day following the Expiration Date as in effect immediately prior to such extension. |

||

|

We may withdraw the Offer and Consent Solicitation only if the conditions of the Offer and Consent Solicitation are not satisfied or waived prior to the Expiration Date. Promptly upon any such withdrawal, we will return the tendered warrants (and the related consent to the Warrant Amendment will be revoked). We will announce our decision to withdraw the Offer and Consent Solicitation by disseminating notice by public announcement or otherwise as permitted by applicable law. See “The Offer and Consent Solicitation — General Terms — Offer Period.” |

||

|

Amendments to the Offer and Consent Solicitation |

We reserve the right at any time or from time to time to amend the Offer and Consent Solicitation, including by increasing or (if the conditions to the Offer are not satisfied) decreasing the exchange ratio of common stock issued for every warrant exchanged or by changing the terms of the Warrant Amendment. If we make a material change in the terms of the Offer and Consent Solicitation or the information concerning the Offer and Consent Solicitation, or if we waive a material condition of the Offer and Consent Solicitation, we will extend the Offer and Consent Solicitation to the extent required by Rules 13e-4(d)(2) and 13e-4(e)(3) under the Exchange Act. See “The Offer and Consent Solicitation — General Terms — Amendments to the Offer and Consent Solicitation.” |

|

|

Conditions to the Offer and Consent Solicitation |

The Offer is subject to customary conditions, including the effectiveness of the registration statement of which this Prospectus/Offer to Exchange forms a part and the absence of any action or proceeding, statute, rule, regulation or order that would challenge or restrict the making or completion of the Offer. The Offer is not conditioned upon the receipt of a minimum number of tendered warrants or the consummation of the Capital Acquisition. However, the Consent Solicitation is conditioned upon receiving the consent of holders of at least 65% of the outstanding public warrants (which is the minimum number required to amend the Warrant Agreement). We may waive some of the conditions to the Offer. See “The Offer and Consent Solicitation — General Terms —Conditions to the Offer and Consent Solicitation.” |

|

Withdrawal Rights |

If you tender your warrants for exchange and change your mind, you may withdraw your tendered warrants (and thereby automatically revoke the related consent to the Warrant Amendment with respect to your public warrants) at any time prior to the Expiration Date, as described in greater detail in the section entitled “The Offer and Consent Solicitation — Withdrawal Rights.” If the Offer Period is extended, you may withdraw your tendered warrants (and thereby automatically revoke the related consent to the Warrant Amendment with respect to your public warrants) at any time until the extended Expiration Date. In addition, tendered warrants that are not accepted by us for exchange by April 26, 2019 may thereafter be withdrawn by you until such time as the warrants are accepted by us for exchange. |

|

Participation by Directors, Executive Officers and Affiliates |

CFLL Sponsor beneficially owns 10,822,500 private placement warrants, or 97.5% of the outstanding private placement warrants. Howard D. Morgan, Heather L. Faust, and Tariq Osman, members of our Board, are managers of CFLL Sponsor and, along with the other managers of CFLL Sponsor Joseph Del Toro and Charles Burns, share voting and investment discretion with respect to the common stock held by CFLL Sponsor. In addition, CFLL Sponsor is 100% owned by funds managed by Argand Partners, LP, which beneficially own more than 5% of the Company. The Company and CFLL Sponsor have entered into the Tender and Support Agreement, pursuant to which CFLL Sponsor has agreed to tender its private placement warrants pursuant to the Offer.

David Hall, David Brown, and Brian Hodges, members of our Board, also each beneficially own 55,500 private placement warrants. Each of Messrs. Hall, Brown and Hodges has indicated to us that he will participate in the Offer, although none of them is required to do so.

None of our other directors, executive officers or affiliates beneficially owns any warrants as of the date of this Offer and Consent Solicitation. See “The Offer and Consent Solicitation – Interests of Directors, Executive Officers and Others.” |

| Federal and State Regulatory Approvals | Other than compliance with the applicable federal and state securities laws, no federal or state regulatory requirements must be complied with and no federal or state regulatory approvals must be obtained in connection with the Offer and Consent Solicitation. |

| Absence of Appraisal or Dissenters’ Rights | Holders of warrants do not have any appraisal or dissenters’ rights under applicable law in connection with the Offer and Consent Solicitation. | ||

|

U.S. Federal Income Tax Consequences of the Offer |

For those holders of warrants participating in the Offer and for any holders of warrants subsequently exchanged for common stock pursuant to the terms of the Warrant Amendment, if approved, we intend to treat your exchange of warrants for our common stock as a “recapitalization” within the meaning of Section 368(a)(1)(E) of the Code pursuant to which (i) you should not recognize any gain or loss on the exchange of warrants for shares of common stock, (ii) your aggregate tax basis in our common stock received in the exchange should equal your aggregate tax basis in your warrants surrendered in the exchange (except to the extent of any tax basis allocated to a fractional share for which a cash payment is received in connection with the Offer), and (iii) your holding period for our common stock received in the exchange should include your holding period for the surrendered warrants. However, because there is a lack of direct legal authority regarding the U.S. federal income tax consequences of the exchange of warrants for our common stock, there can be no assurance in this regard and alternative characterizations are possible by the IRS or a court, including ones that would require U.S. holders to recognize taxable income. |

||

|

Although the issue is not free from doubt, we intend to treat all warrants not exchanged for common stock in the Offer as having been exchanged for “new” warrants pursuant to the Warrant Amendment and to treat such deemed exchange as a “recapitalization” within the meaning of Section 368(a)(1)(E) of the Code, pursuant to which (i) you should not recognize any gain or loss on the deemed exchange of warrants for “new” warrants, (ii) your aggregate tax basis in the “new” warrants deemed to be received in the exchange should equal your aggregate tax basis in your existing warrants surrendered in the exchange, and (iii) your holding period for the “new” warrants deemed to be received in the exchange should include your holding period for the surrendered warrants. Because there is a lack of direct legal authority regarding the U.S. federal income tax consequences of the deemed exchange of warrants for “new” warrants pursuant to the Warrant Amendment, if approved, there can be no assurance in this regard and alternative characterizations by the IRS or a court are possible, including ones that would require U.S. holders to recognize taxable income. See “The Offer — Material U.S. Federal Income Tax Consequences.” |

|||

|

No Recommendation |

None of our Board, our management, the dealer manager, the exchange agent, the information agent or any other person makes any recommendation on whether you should tender or refrain from tendering all or any portion of your warrants or consent to the Warrant Amendment, and no one has been authorized by any of them to make such a recommendation. |

||

|

Risk Factors |

For risks related to the Offer and Consent Solicitation, please read the section entitled “Risk Factors” in of this Prospectus/Offer to Exchange. |

||

|

Exchange Agent |

The depositary and exchange agent for the Offer and Consent Solicitation is:

Continental Stock Transfer & Trust Company 1 State Street, 30th Floor New York, NY 10004 Facsimile: (212) 616-7616 |

||

|

Dealer Manager |

The dealer manager for the Offer and Consent Solicitation is:

UBS Securities LLC 1285 Avenue of the Americas New York, New York 10019 Attention: Equity Capital Markets (212) 713-2626 |

|

|

We have other business relationships with the dealer manager, as described in “The Offer and Consent Solicitation — Dealer Manager.” |

||

|

Additional Information |

We recommend that our warrant holders review the registration statement on Form S-4, of which this Prospectus/Offer to Exchange forms a part, including the exhibits that we have filed with the SEC in connection with the Offer and Consent Solicitation and our other materials that we have filed with the SEC, before making a decision on whether to tender for exchange in the Offer and consent to the Warrant Amendment. All reports and other documents we have filed with the SEC can be accessed electronically on the SEC’s website at www.sec.gov. |

|

|

You should direct (1) questions about the terms of the Offer and Consent Solicitation to the dealer manager at its addresses and telephone number listed above and (2) questions about the exchange procedures and requests for additional copies of this Prospectus/Offer to Exchange, the Letter of Transmittal and Consent or Notice of Guaranteed Delivery to the information agent at the below address and phone number:

Morrow Sodali LLC 470 West Avenue Stamford, Connecticut 06902 Individuals, please call toll-free: (800) 662-5200 Banks and brokerage firms, please call: (203) 658-9400 Email: BBCP.info@morrowsodali.com |

||

|

Successor |

Predecessor |

|||||||||||||||||||||||

| December 6, 2018 | November 1, 2018 | November 1, 2017 | ||||||||||||||||||||||

| through | through | through |

Year Ended October 31, |

|||||||||||||||||||||

|

(in thousands) |

January 31, 2019 |

December 5, 2018 |

January 31, 2018 |

2018 |

2017 |

2016 |

||||||||||||||||||

| (unaudited) | (unaudited) | (unaudited) | ||||||||||||||||||||||

|

Statement of operations data |

||||||||||||||||||||||||

|

Revenue |

$ | 33,970 | $ | 24,396 | $ | 52,802 | $ | 243,223 | $ | 211,211 | $ | 172,426 | ||||||||||||

|

Operating (loss) income |

(814 |

) |

(8,734 |

) |

9,089 | 39,967 | 32,405 | 30,902 | ||||||||||||||||

|

Net (loss) income |

$ | (3,630 |

) |

$ | (22,575 |

) |

$ | 17,558 | $ | 28,381 | $ | 913 | $ | 6,234 | ||||||||||

|

Net (loss) income per share-basic |

$ | (0.14 |

) |

$ | (3.00 |

) |

$ | 1.74 | $ | 2.72 | $ | (0.12 |

) |

$ | 0.46 | |||||||||

|

Net (loss) income per share-diluted |

$ | (0.14 |

) |

$ | (3.00 |

) |

$ | 1.55 | $ | 2.47 | $ | (0.12 |

) |

$ | 0.42 | |||||||||

|

Successor |

Predecessor |

|||||||||||||||

|

As of January 31, |

As of October 31, |

|||||||||||||||

|

2019 |

2018 |

2017 |

2016 |

|||||||||||||

| (in thousands) | (unaudited) | |||||||||||||||

|

Balance sheet data: |

||||||||||||||||

|

Cash and cash equivalents |

$ | 4,767 | $ | 8,621 | $ | 6,925 | $ | 3,249 | ||||||||

|

Total assets |

$ | 735,448 | $ | 370,144 | $ | 338,847 | $ | 254,929 | ||||||||

|

Total current liabilities |

$ | 66,791 | $ | 94,950 | $ | 96,302 | $ | 31,583 | ||||||||

|

Total long term liabilities |

$ | 397,044 | $ | 214,501 | $ | 208,717 | $ | 186,249 | ||||||||

| Redeemable convertible preferred stock (mezzanine equity) | $ | 25,000 | $ | 14,672 | $ | 14,672 | $ | 15,182 | ||||||||

|

Total stockholders’ equity |

$ | 246,613 | $ | 46,021 | $ | 19,156 | $ | 21,915 | ||||||||

|

Successor |

Predecessor |

|||||||||||||||||||||||

|

December 6, 2018 |

November 1, 2018 |

November 1, 2017 |

||||||||||||||||||||||

| through | through | through |

Year Ended October 31, |

|||||||||||||||||||||

|

January 31, 2019 |

December 5, 2018 |

January 31, 2018 |

2018 |

2017 |

2016 |

|||||||||||||||||||

|

(in thousands) |

||||||||||||||||||||||||

|

Other financial data (unaudited): |

||||||||||||||||||||||||

|

Adjusted EBITDA(1) |

$ | 7,560 | $ | 9,588 | $ | 16,371 | $ | 78,868 | $ | 68,364 | $ | 59,644 | ||||||||||||

|

(1) Adjusted EBITDA measures performance by adjusting EBITDA for certain income and expense items that are not considered part of CPH’s core operations. See “Non-GAAP Measures (Adjusted EBITDA)” below for an explanation of this measure and reconciliation to net income, the most comparable GAAP measure. |

| Non-GAAP Measures (Adjusted EBITDA) |

| We calculate EBITDA by taking GAAP net income and adding back interest expense, net, income taxes, depreciation and amortization. Adjusted EBITDA is calculated by taking EBITDA and adding back transaction expenses, other adjustments, management fees and other expenses. We believe these non-GAAP measures of financial results provide useful information to management and investors regarding certain financial and business trends related to our financial condition and results of operations, as a tool for investors to use in evaluating our ongoing operating results and trends and in comparing our financial measures with competitors who also present similar non-GAAP financial measures. In addition, these measures (1) are used in quarterly financial reports prepared for management and our Board and (2) help management to determine incentive compensation. EBITDA and Adjusted EBITDA have limitations and should not be considered in isolation or as a substitute for performance measures calculated under GAAP. This non-GAAP measure excludes certain cash expenses that we are obligated to make. In addition, other companies in our industry may calculate EBITDA and Adjusted EBITDA differently or may not calculate it at all, which limits the usefulness of EBITDA and Adjusted EBITDA as comparative measures. |

| The following table presents a reconciliation of our consolidated net income (loss) to EBITDA and Adjusted EBITDA: |

|

Successor |

Predecessor |

|||||||||||||||||||||||

|

December 6, 2018 |

November 1, 2018 |

|||||||||||||||||||||||

|

through |

through |

Three months ended |

Years Ended October 31, |

|||||||||||||||||||||

|

January 31, 2019 |

December 5, 2018 |

January 31, 2018 |

2018 |

2017 |

2016 |

|||||||||||||||||||

|

Statement of operations information: |

||||||||||||||||||||||||

|

Net income (loss) |

$ | (3,630 | ) | $ | (22,575 | ) | $ | 17,558 | $ | 28,382 | $ | 913 | $ | 6,234 | ||||||||||

|

Interest expense, net |

5,592 | 1,644 | 5,087 | 21,425 | 22,748 | 19,516 | ||||||||||||||||||

|

Income tax (benefit) expense |

(2,765 | ) | (4,192 | ) | (13,544 | ) | (9,784 | ) | 3,757 | 4,454 | ||||||||||||||

|

Depreciation and amortization |

8,374 | 2,713 | 5,950 | 25,623 | 27,154 | 22,310 | ||||||||||||||||||

|

EBITDA |

7,571 | (22,410 | ) | 15,051 | 65,646 | 54,572 | 52,514 | |||||||||||||||||

|

Transaction expenses(1) |

- | 14,167 | 8 | 7,590 | 4,490 | 3,691 | ||||||||||||||||||

|

Loss on debt extinguishment |

- | 16,395 | - | - | 5,161 | 644 | ||||||||||||||||||

|

Other (income) expense |

(11 | ) | (6 | ) | (12 | ) | (55 | ) | (174 | ) | 54 | |||||||||||||

|

Other adjustments(2) |

- | 1,442 | 1,324 | 5,687 | 4,315 | 2,741 | ||||||||||||||||||

|

Adjusted EBITDA |

$ | 7,560 | $ | 9,588 | $ | 16,371 | $ | 78,868 | $ | 68,364 | $ | 59,644 | ||||||||||||

|

(1) |

Transaction expenses represented expenses incurred for legal, accounting, and other professionals that were engaged in the completion of various acquisitions. |

|

(2) |

Other adjustments include severance expenses, senior executive relocation costs, management fees, recruiting costs and non-cash expenses such as stock-based compensation. |

SUMMARY UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION

The following summary unaudited pro forma combined statement of operations data for the three months ended January 31, 2019 (on a combined basis with respect to Predecessor and Successor periods) and year ended October 31, 2018 presents our combined unaudited results of operations after giving effect (i) to the Capital Acquisition and (ii) the Business Combination, as if each had been completed as of November 1, 2017. The following pro forma combined balance sheet data presents our combined financial position as of January 31, 2019 after giving effect to (i) the Capital Acquisition as if it had been completed as of January 31, 2019. The summary unaudited pro forma condensed consolidated financial data has been prepared from, and should be read in conjunction with, the unaudited pro forma condensed combined financial information set forth under the caption “Unaudited Pro Forma Condensed Combined Financial Information” and the historical consolidated financial statements and notes thereto of the Company and the historical consolidated financial statements of the Capital Companies, each included elsewhere in this Prospectus/Offer to Exchange.

The summary historical profit and loss accounts of each of these entities have been prepared in accordance with U.S. GAAP. The pro forma acquisition adjustments described in the summary unaudited pro forma condensed consolidated financial information are based on available information and certain assumptions made by us and may be revised as additional information becomes available as the purchase accounting for the acquisition is finalized. The pro forma adjustments are based on preliminary estimates of the fair values of assets acquired and information available as of the date of this Prospectus/Offer to Exchange. Certain valuations are currently in process. Actual results may differ from the amounts reflected in the unaudited pro forma condensed consolidated financial statements, and the differences may be material.

The unaudited pro forma condensed consolidated financial information included in this Prospectus/Offer to Exchange is not intended to represent what our results of operations would have been if the Capital Acquisition and the Business Combination had occurred on November 1, 2017 (or January 31, 2019) or to project our results of operations for any future period. Therefore, the unaudited pro forma condensed consolidated financial results may not be comparable to, or indicative of, future performance.

This pro forma information is subject to risks and uncertainties, including those discussed in “Risk Factors.”

|

SUMMARY UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

||||||||

|

Summary Unaudited Pro Forma Condensed Combined Statement of Operations Information |

||||||||

|

(in thousands, except share and per share data) |

Three Months Ended January 31, 2019 |

Year Ended October 31, 2018 |

||||||

|

Revenue |

$ | 70,332 | $ | 292,753 | ||||

|

Net (loss) income available to common shareholders |

$ | (16,702 | ) | $ | 12,808 | |||

|

Basic (loss) earnings per share from continuing operations available to common stockholders |

$ | (0.43 | ) | $ | 0.33 | |||

|

Diluted (loss) earnings per share from continuing operations available to common stockholders |

$ | (0.43 | ) | $ | 0.31 | |||

|

Weighted average shares outstanding – Basic |

39,275 | 39,275 | ||||||

|

Weighted average shares outstanding – Diluted |

39,275 | 41,643 | ||||||

|

Summary Unaudited Pro Forma Condensed Combined Balance Sheet Information |

||||||||

|

(in thousands, except share and per share data) |

As of |

|||||||

|

Total assets |

$ | 865,938 | ||||||

|

Redeemable convertible preferred stock (mezzanine equity) |

$ | 25,000 | ||||||

|

Total stockholders’ equity |

$ | 339,203 | ||||||

|

Total liabilities and stockholders’ equity |

$ | 865,938 | ||||||

An investment in any securities offered pursuant to this Prospectus/Offer to Exchange involves risk and uncertainties. You should consider carefully the risk factors below and the risks described in the proxy statement/prospectus, our most recent Annual Report on Form 10-K, our most recent Quarterly Report on Form 10-Q and any subsequent Quarterly Reports on Form 10-Q and Current Reports on Form 8-K filed with the SEC we file after the date of this Prospectus/Offer to Exchange, as well as the other information contained in this Prospectus/Offer to Exchange, and any applicable prospectus supplement, before making an investment decision. Any of the risk factors could significantly and negatively affect our business, financial condition, results of operations, cash flows, and prospects and the trading price of our securities. You could lose all or part of your investment.

Risks Related to our Business and Operations

Our business is cyclical in nature and a slowdown in the economic recovery or a decrease in general economic activity could have a material adverse effect on our revenues and operating results.

Substantially all of our customer base comes from the commercial, infrastructure and residential construction sectors. A worsening of economic conditions or a decrease in available capital for investments could cause weakness in our end markets, cause declines in construction and industrial activity, and adversely affect our revenue and operating results.

The following factors, among others, may cause weakness in our end markets, either temporarily or long-term:

|

● |

the depth and duration of an economic downturn and lack of availability of credit; |

|

|

● |

uncertainty regarding global, regional or sovereign economic conditions; |

|

|

● |

reductions in corporate spending for plants and facilities or government spending for infrastructure projects; |

|

|

● |

the cyclical nature of our customers’ businesses, particularly those operating in the commercial, infrastructure and residential construction sectors; |

|

|

● |

an increase in the cost of construction materials; |

|

|

● |

a decrease in investment in certain of our key geographic regions; |

|

|

● |

an increase in interest rates; |

|

|

● |

an overcapacity in the businesses that drive the need for construction; |

|

|

● |

adverse weather conditions, which may temporarily affect a particular region or regions; |

|

|

● |

reduced construction activity in our end markets; |

|

|

● |

terrorism or hostilities involving the United States or the United Kingdom; |

|

|

● |

change in structural construction designs of buildings (e.g., wood versus concrete); |

|

|

● |

negative impact on our U.K. business as a result of Brexit; and |

|

|

● |

oversupply of equipment or new entrants into the market causing pricing pressure. |

A downturn in any of our end markets in one or more of our geographic regions caused by these or other factors could have a material adverse effect on our business, financial conditions, results of operations and cash flows.

Our business is seasonal and subject to adverse weather.

Since our business is primarily conducted outdoors, erratic weather patterns, seasonal changes and other weather related conditions affect our business. Adverse weather conditions, including hurricanes and tropical storms, cold weather, snow, and heavy or sustained rainfall, reduce construction activity, restrict the demand for our products and services, and impede our ability to deliver and pump concrete efficiently or at all. In addition, severe drought conditions can restrict available water supplies and restrict production. Consequently, these events could adversely affect our business, financial condition, results of operations, liquidity and cash flows.

Our revenue and operating results have varied historically from period to period and any unexpected periods of decline could result in an overall decline in our available cash flows.

Our revenue and operating results have varied historically from period to period and may continue to do so. We have identified below certain of the factors that may cause our revenue and operating results to vary:

|

● |

seasonal weather patterns in the construction industry on which we rely, with activity tending to be lowest in the winter and spring; |

|

|

● |

the timing of expenditure for maintaining existing equipment, new equipment and the disposal of used equipment; |

|

|

● |

changes in demand for our services or the prices we charge due to changes in economic conditions, competition or other factors; |

|

|

● |

changes in the interest rates applicable to our variable rate debt, and the overall level of our debt; |

|

|

● |

fluctuations in fuel costs; |

|

|

● |

general economic conditions in the sectors where we operate; |

|

|

● |

the cyclical nature of our customers’ businesses; |

|

|

● |

price changes in response to competitive factors; |

|

|

● |

other cost fluctuations, such as costs for employee-related compensation and benefits; |

|

|

● |

labor shortages, work stoppages or other labor difficulties and labor issues in trades on which our business may be dependent in particular regions; |

|

|

● |

potential enactment of new legislation affecting our operations or labor relations; |

|

|

● |

timing of acquisitions and new branch openings and related costs; |

|

|

● |

possible unrecorded liabilities of acquired companies and difficulties associated with integrating acquired companies into our existing operations; |

|

|

● |

changes in the exchange rate between the United States dollar and Great Britain pound sterling; |

|

|

● |

potential increased demand from our customers to develop and provide new technological services in our business to meet changing customer preferences; |

|

|

● |

our ability to control costs and maintain quality; |

|

|

● |

our effectiveness in integrating new locations and acquisitions; and |

|

|

● |

possible write-offs or exceptional charges due to changes in applicable accounting standards, goodwill impairments, reorganizations or restructurings, obsolete or damaged equipment or the refinancing of our existing debt. |

Our business is highly competitive and competition may increase, which could have a material adverse effect on our business.

The concrete pumping industry is highly competitive and fragmented. Many of the markets in which we operate are served by several competitors, ranging from larger regional companies to small, independent businesses with a limited fleet and geographic scope of operations. Some of our principal competitors may have more flexible capital structures or may have greater name recognition in one or more of our geographic markets and may be better able to withstand adverse market conditions within the industry. We generally compete on the basis of, among other things, quality and breadth of service, expertise, reliability, price and the size, quality and availability of our fleet of pumping equipment, which is significantly affected by the level of our capital expenditures. If we are required to reduce or delay capital expenditures for any reason, including due to restrictions contained in, or debt service payments required by, our credit facilities or otherwise, or due to the use of cash for acquisitions, the ability to replace our fleet or the age of our fleet may put us at a disadvantage to our competitors and adversely impact our ability to generate revenue. In addition, our industry may be subject to competitive price decreases in the future, particularly during cyclical downturns in our end markets, which can adversely affect revenue, profitability and cash flow. We may encounter increased competition from existing competitors or new market entrants in the future, which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We are dependent on our relationships with key suppliers to obtain equipment for our business.

We depend on a small group of key manufacturers of concrete pumping equipment, and has historically relied primarily on three companies, the largest two of which experienced ownership changes in 2012. We cannot predict the impact on our suppliers of changes in the economic environment and other developments in their respective businesses, and we cannot provide any assurance that our vendors will provide their historically high level of service support and quality. Any deterioration in such service support or quality could result in additional maintenance costs, operational issues, or both. Insolvency, financial difficulties, strategic changes or other factors may result in our suppliers not being able to fulfill the terms of their agreements with us, whether satisfactorily or at all. Further, such factors may render suppliers unwilling to extend contracts that provide favorable terms to us, or may force them to seek to renegotiate existing contracts with us. We believe the market for supplying equipment used in our business is increasingly competitive; however, termination of our relationship with any of our key suppliers, or interruption of our access to concrete pumping equipment, pipe or other supplies, could have a material adverse effect on our business, financial condition, results of operations and cash flows in the event that we are unable to obtain adequate and reliable equipment or supplies from other sources in a timely manner or at all.

If our average fleet age increases, our offerings may not be as attractive to potential customers and our operating costs may increase, impacting our results of operations.

As our equipment ages, the cost of maintaining such equipment, if not replaced within a certain period of time or amount of use, will likely increase. We estimate that our fleet assets generally will have a useful life of up to 25 years depending on the size of the machine, hours in service, yardage pumped, and, in certain instances, other circumstances unique to an asset. We manage our fleet of equipment according to the wear and tear that a specific type of equipment is expected to experience over its useful life. As of January 31, 2019, the average age of our equipment was approximately 9 years, and it is our strategy to maintain average fleet age at approximately 10 years. If the average age of our equipment increases, whether as a result of our inability to access sufficient capital to maintain or replace equipment in a timely manner or otherwise, our investment in the maintenance, parts and repair for individual pieces of equipment may exceed the book value or replacement value of that equipment. We cannot assure you that costs of maintenance will not materially increase in the future. Any material increase in such costs could have a material adverse effect on our business, financial condition and results of operations. Additionally, as our equipment ages, it may become less attractive to potential customers, thus decreasing our ability to effectively compete for new business.

The costs of new equipment we use in our fleet may increase, requiring us to spend more for replacement equipment or preventing us from procuring equipment on a timely basis.

The cost of new equipment for use in our concrete pumping fleet could increase due to increased material costs to our suppliers or other factors beyond our control. Such increases could materially adversely impact our financial condition, results of operations and cash flows in future periods. Furthermore, changes in technology or customer demand could cause certain of our existing equipment to become obsolete and require us to purchase new equipment at increased costs.

We sell used equipment on a regular basis. Our fleet is subject to residual value risk upon disposition, and may not sell at the prices or in the quantities we expect.

We continuously evaluate our fleet of equipment as we seek to optimize our vehicle size and capabilities for our end markets in multiple locations. We therefore seek to sell used equipment on a regular basis. The market value of any given piece of equipment could be less than its depreciated value at the time it is sold. The market value of used equipment depends on several factors, including:

|

● |

the market price for comparable new equipment; |

|

|

● |

wear and tear on the equipment relative to its age and the effectiveness of preventive maintenance; |

|

|

● |

the time of year that it is sold; |

|

|

● |

the supply of similar used equipment on the market; |

|

|

● |

the existence and capacities of different sales outlets; |

|

|

● |

the age of the equipment, and the amount of usage of such equipment relative to its age, at the time it is sold; |

|

|

● |

worldwide and domestic demand for used equipment; |

|

|

● |

the effect of advances and changes in technology in new equipment models; |

|

|

● |

changing perception of residual value of used equipment by our suppliers; and |

|

|

● |

general economic conditions. |

We include in income from operations the difference between the sales price and the depreciated value of an item of equipment sold. Changes in our assumptions regarding depreciation could change our depreciation expense, as well as the gain or loss realized upon disposal of equipment. Sales of our used concrete pumping equipment at prices that fall significantly below our expectations or in lesser quantities than we anticipate could have a negative impact on our financial condition, results of operations and cash flows.

We are exposed to liability claims on a continuing basis, which may exceed the level of our insurance or not be covered at all, and this could have a material adverse effect on our operating performance.

Our business exposes itself to claims for personal injury, death or property damage resulting from the use of the equipment we operate, rent, sell, service or repair and from injuries caused in motor vehicle or other accidents in which our personnel are involved. Our business also exposes it to worker compensation claims and other employment-related claims. We carry comprehensive insurance, subject to deductibles, at levels we believe are sufficient to cover existing and future claims. Future claims may exceed the level of our insurance, and our insurance may not continue to be available on economically reasonable terms, or at all. Certain types of claims, such as claims for punitive damages, are not covered by our insurance. In addition, we are self-insured for the deductibles on our policies and have established reserves for incurred but not reported claims. If actual claims exceed our reserves, our results of operations could be adversely affected. Whether or not we are covered by insurance, certain claims may generate negative publicity, which may lead to lower revenues, as well as additional similar claims being filed.

Our business is subject to significant operating risks and hazards that could result in personal injury or damage or destruction to property, which could result in losses or liabilities to us.

Construction sites are potentially dangerous workplaces and often put our employees and others in close proximity with mechanized equipment and moving vehicles. Our equipment has been involved in workplace incidents and incidents involving mobile operators of our equipment in transit in the past and may be involved in such incidents in the future.

Our safety record is an important consideration for us and for our customers. If serious accidents or fatalities occur, regardless of whether we were at fault, or our safety record were to deteriorate, we may be ineligible to bid on certain work, be exposed to possible litigation, and existing service arrangements could be terminated, which could have a material adverse impact on our financial position, results of operations, cash flows and liquidity. Adverse experience with hazards and claims could have a negative effect on our reputation with our existing or potential new customers and our prospects for future work.

In the commercial concrete infrastructure sector, our workers are subject to the usual hazards associated with providing construction and related services on construction sites, including environmental hazards, industrial accidents, hurricanes, adverse weather conditions and flooding. Operating hazards can cause personal injury or death, damage to or destruction of property, plant and equipment, environmental damage, performance delays, monetary losses or legal liability.

Potential acquisitions and expansions into new markets may result in significant transaction expense and expose us to risks associated with entering new markets and integrating new or acquired operations.

We may encounter risks associated with entering new markets in which we have limited or no experience. New operations require significant capital expenditures and may initially have a negative impact on our short-term cash flow, net income and results of operations. New start-up locations may not become profitable when projected or ever. In addition, our industry is highly fragmented and we expect to consider acquisition opportunities from time to time when we believe they would enhance our business and financial performance.

Acquisitions, such as the Capital Acquisition, may impose significant strains on our management, operating systems and financial resources, and could experience unanticipated integration issues. The pursuit and integration of acquisitions, such as the Capital Acquisition, may require substantial attention from our senior management, which will limit the amount of time they have available to devote to our existing operations. Our ability to realize the expected benefits from any future acquisitions, such as the Capital Acquisition, depends in large part on our ability to integrate and consolidate the new operations with our existing operations in a timely and effective manner. Future acquisitions, such as the Capital Acquisition, also could result in the incurrence of substantial amounts of indebtedness and contingent liabilities (including environmental, employee benefits and safety and health liabilities), accumulation of goodwill that may become impaired, an increase in amortization expenses related to intangible assets, and potential penalties or other break fees if such negotiated acquisitions are not consummated. Any significant diversion of management’s attention from our existing operations, the loss of key employees or customers of any acquired business, any major difficulties encountered in the opening of start-up locations or the integration of acquired operations or any associated increases in indebtedness, liabilities or expenses could have a material adverse effect on our business, financial condition or results of operations.

We may not realize the anticipated synergies and cost savings from acquisitions.

We have completed a number of acquisitions in recent years that we believe present revenue and cost-saving synergy opportunities and we expect to realize significant synergies from the Capital Acquisition. However, the integration of recent or future acquisitions may not result in the realization of the full benefits of the revenue and cost synergies that we expected at the time or currently expect within the anticipated time frame or at all. Moreover, we may incur substantial expenses or unforeseen liabilities in connection with the integration of acquired businesses, including in connection with the Capital Acquisition. While we anticipate that certain expenses will be incurred, such expenses are difficult to estimate accurately and may exceed our estimates. Accordingly, the expected benefits may be offset by costs or delays incurred in integrating the businesses. Failure of recent or future acquisitions to meet our expectations and be integrated successfully could have a material adverse effect on our financial condition and results of operations.